The Shocking Truth About Your Credit Score

The Shocking Truth About Your Credit Score

Secret to skyrocketing!

The party starts now that you are here. Let's get this article on the internet!

Pixsy empowers you to discover unauthorized usage of your cherished photographs on the vast expanse of the internet.

In Today’s Email:

Unlocking the Mystery of Credit Scores

Fun Finds

Ending on a High Note…

Unlocking the Mystery of Credit Scores

The CIBIL score. Three little words strike fear into the hearts of borrowers, yet hold the key to financial freedom. It's a number that can make or break your loan application, determine the interest rate on your credit card, and even affect your ability for a mortgage. The struggle is real for those who have felt the sting of a low score. But fear not, understanding the CIBIL score is the first step towards taking control of your financial destiny.

Credit scores are a numerical representation of a borrower's creditworthiness. The score is based on a number of factors, including payment history, credit utilization, length of credit history, new credit, and credit mix. Credit scores range from 350 to 900, with higher scores indicating better creditworthiness.

If your credit score is at least 750, you will be eligible for the highest number of credit cards and you will also have a greater likelihood of being approved for any loan.

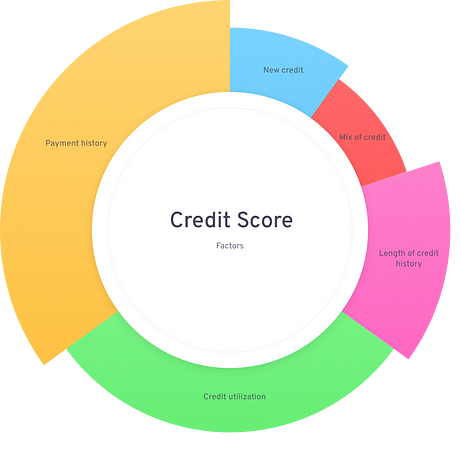

What be the constituents of your credit score?

Payment History (35%)

When it comes to tallying up your creditworthiness, nothing weighs heavier than your payment history. A single slip-up, whether it be small or big, can drag your score through the mud. What's more, it signals to potential lenders that you may default on payments down the line. To keep your credit score shining, pay your dues promptly and keep those loans and cards in check.

Credit Utilization (30%)

Credit utilization measures how much of your plastic you've spent in a month, divided by your total credit limit. Say your credit limit is a cool one lakh, and you've spent fifty thousand - then your utilization hits 50%. But if you're maxing out your limit, you're telling lenders you're not the best at handling your money. So, to keep creditors off your back, don't blow your entire credit limit.

Length of Credit History (15%)

Your age doesn't count for squat when credit bureaus calculate your score, but the length of your credit history sure does. They take into account the span between your first and most recent loans or cards, and the average age of all your accounts put together. The longer your first account has been open, the better your score.

Mix of Credit (10%)

Your mix of credit describes the variety of accounts listed on your credit report. There are two kinds of credit accounts: instalment-based loans and revolving credit cards. When you've got a mix of both, it shows lenders you can handle all sorts of credit products. And that makes you a good catch in their eyes.

For eg., a mortgage loan, personal loan or consumer loan, credit cards etc.,

New Credit (10%)

Your recent credit history depends on the number of fresh accounts you've opened and the credit schemes you've sought after. Each time you request a loan or card, the lender's inquiry goes hard. That means they peek at your credit report from the bureaus to rate your score and trustworthiness. Soft inquiries - when you check your score yourself - don't affect your credit, but too many hard ones over a short period sure can. It'll tank your score in no time flat.

What's in your credit report?

Basic identification information

A list of your credit accounts

Your credit history (whom you’ve paid, how consistently you paid, and any late payments)

Amount of loans

Credit inquiries or who else has requested your credit information (e.g., other lenders)

Your choices affect your credit score

Consider two friends, Friend 1 and Friend 2, each earning about 18 lakhs a year.

Friend 1 is diligent, setting aside a portion of their earnings each month and consistently meeting their credit card and mortgage payments. Meanwhile,

Friend 2 lives recklessly, exceeding their financial means, pushing their credit limits, and missing payments on occasion.

Friend 1 and Friend 2 both applied for a loan at the bank. In light of their financial backgrounds, who do you think would be granted approval or a favourable interest rate?

It is more likely that Friend 1 would be granted loan approval or receive a better interest rate from the bank. This is because lenders typically favour individuals with a positive credit history and a proven track record of financial responsibility. On the other hand, Friend 2's poor credit history and missed payments could result in a higher interest rate or even loan denial.

To save time, lenders created the credit score, which considers your complete financial background. Obtaining and utilizing a credit card is the simplest way to begin establishing your credit score.

Boost thy credit score: a concise guide

Get out of unnecessary debt fast

Keep your accounts open

Keep your utilization ratio around 5-10% and never cross more than 30%

Never miss a payment and always pay in full every month

Start using a credit card and never unconsciously apply for another credit card when you don’t need one.

Fun Finds

Food

The Whole Truth, is a brand that offers 100% natural products that are clean and delicious. They use high-quality, all-natural ingredients in protein bars, muesli, nut butter, and chocolates. Products are free from any added artificial sugar, preservatives, or chemicals. Whether you need a quick snack on the go or a healthy dessert, The Whole Truth has got you covered.Product

Minimalist, created this simple yet effective skincare line to make you feel like a confident and self-assured person who values a minimal approach to skincare. This is one of the few skincare products I've found that actually keeps my skin hydrated and refreshed, while also keeping my conscience clear with its ingredients. Plus, it won't break the bank, as it is priced affordably for everyone to enjoy.

Ending on a High Note…

Looking to simplify your life and find true happiness? Look no further than The Minimalists: Less Is Now, a powerful and thought-provoking documentary now streaming on Netflix. Join the Minimalists, Joshua Fields Millburn and Ryan Nicodemus, as they explore the transformative power of living with less and delve into the surprising benefits of minimalism.

Bragging Rights

A few years ago, I decided I wanted to improve my financial situation and make more money by investing. I was tired of struggling to get by with each paycheck, and I tried different methods to control my spending and find the best investment strategy. Unfortunately, these methods didn't work out and left me feeling frustrated. I was worried that if I made a bad budget, I might end up worse off than before.

However, I realized that I needed to focus on my values and figure out what was most important to me. I also noticed that budgets often fail for certain reasons, so I made sure to address those issues before they became a problem. The result was a Budget Template that was easy to use and adjust as needed, along with a straightforward guide to analyzing stocks.

The result? My simple and customisable Budget Template and a No-nonsense guide to stock analysis. Join me, won't you?

Instagram: gbrohit